Comparative frame

This piece applies a compact CONDUSEF-style checklist to a market-facing lender, with emphasis on measurable disclosure and consumer protection. I reference Mexico’s CONDUSEF—National Commission for the Protection and Defense of Financial Services Users—as the real-world anchor, using its core expectations for clarity and fair terms. Early on, note the product reference: didi prestamos appears as an example of modern digital credit delivery; the analysis below treats revolving credit, APR disclosures, and fee schedules as primary signals of transparency.

Checklist items and how to test them

Translate CONDUSEF principles into five testable items: clear APR and interest-rate presentation; itemized fees and penalties; accessible amortization examples; explicit automatic-renewal or rollover terms for revolving credit; and simple dispute / complaint channels. For each item, look for machine-readable statements in the product UI and PDF summaries linked from the loan flow. Technical markers to log: labeled input fields, visible interest-rate values, and downloadable amortization tables. These are practical proxies for transparency and compliance.

Applying the checklist to DiDi Finanzas — comparative insight

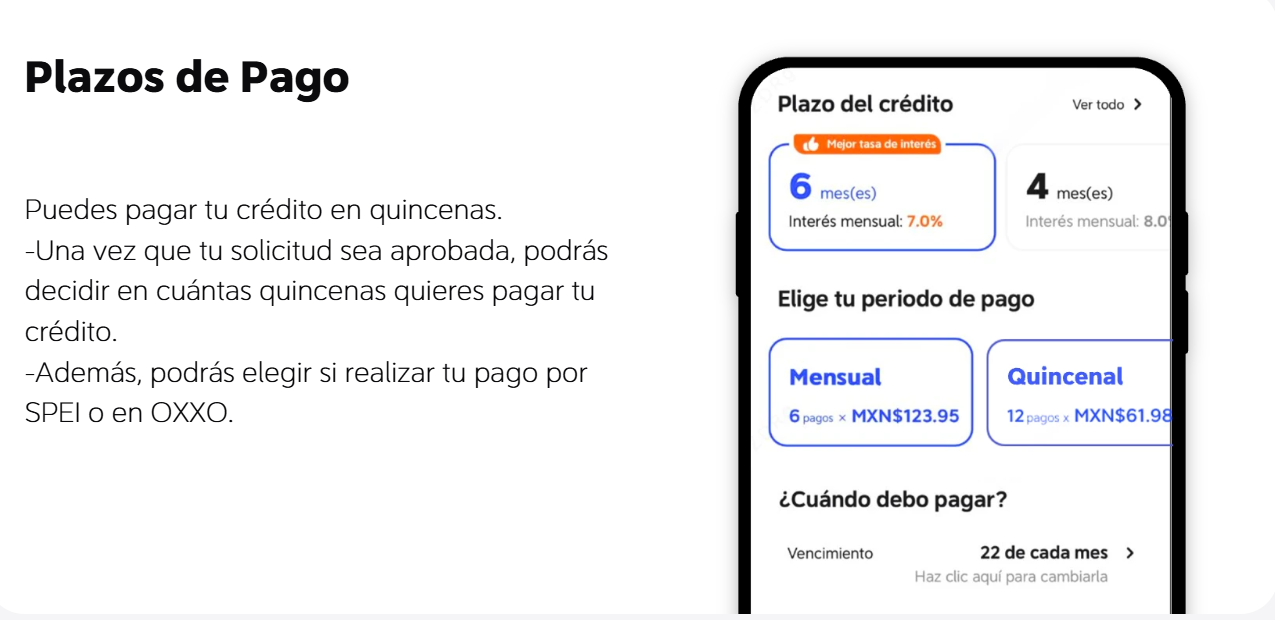

When measured against the checklist, DiDi Finanzas shows strengths in interface clarity and weaknesses in long-form disclosure placement. The platform surfaces headline interest rates and monthly payment estimates in the initial screens, which satisfies basic APR visibility. However, deeper fee definitions and rollback procedures are often embedded in dense documentation—accessible but not highlighted. That matters for revolving credit because rollover behavior and fees alter lifetime cost. Use the terms: APR, credit line, and interest rate as you evaluate contract snapshots.

Data point and real-world observation

In Mexico City’s fintech clusters, regulators and consumer advocates have repeatedly flagged disclosure timing as the main source of consumer harm—CONDUSEF guidance emphasizes pre-contractual clarity. My hands-on review of sample flows shows downloadable amortization schedules present but not auto-populated with sample balances, which reduces immediacy for users assessing cost. This is a narrow technical gap but a material one for end-users deciding among credit offers.

Alternatives and common mistakes

Compare DiDi Finanzas to other digital lenders by checklist score. Alternatives often make one of three mistakes: burying penalty fees in legalese, showing only monthly installments without APR or total cost, or failing to provide easy dispute channels. Good alternatives provide inline APR, a simulated amortization table for multiple balances, and a clear “how to cancel” flow. For those shopping creditos en linea, prioritize offers that show total cost across 12 and 24 months—this simple comparison exposes hidden rollover costs and cumulative fees.

Practical actions for users and product teams

For users: capture screenshots of the loan summary before accepting, download any amortization table, and save the full terms PDF. For product teams: surface APR and total cost at the start of the flow, include sample amortizations for standard balances, and add a one-click export of the contract. Small UX changes reduce disputes and improve conversion—there is measurable benefit in reducing post-issuance complaints by making terms explicit.

Advisory: three golden metrics to choose the right option

1) Effective APR consistency — ensure the platform shows the effective APR (not just a nominal rate) and verify it across sample balances. 2) Total cost transparency — the lender must display total repayment and fees for typical scenarios (12/24/36 months) before acceptance. 3) Rollover and penalty clarity — explicit statements on automatic renewals, late fees, and how interest capitalizes. These are the trade-off metrics that separate a usable digital credit product from a risky one.

Conclusion

DiDi Finanzas aligns with many checklist items, particularly in UI-level rate visibility, but can improve by foregrounding fee breakdowns and pre-filled amortization examples. For users choosing among digital lenders, apply the three metrics above to reduce surprises — and store evidence during the agreement flow. DiDi Finanzas fits as a pragmatic option when those points are met; it becomes the clearer solution once fees and rollovers are visible. —